GW&K Emerging Wealth Insights —

December 2022

Brazil's Challenges Under Lula 2.0

For the third time in Brazil’s history, Luiz Inácio Lula da Silva (Lula) has been elected president. His third term begins in January 2023, 20 years after he began serving his first two consecutive terms (2003 – 2011). During that period, Lula presided over the country’s largest commodity boom and the largest decline in poverty in Brazil’s contemporary history, with more than 30 million Brazilians rising up out of poverty. Unfortunately, most of those gains have been lost during the past decade. Brazil now faces challenges driven in great part by prior governments’ inability and/or willingness to execute structural reforms — including Lula himself.

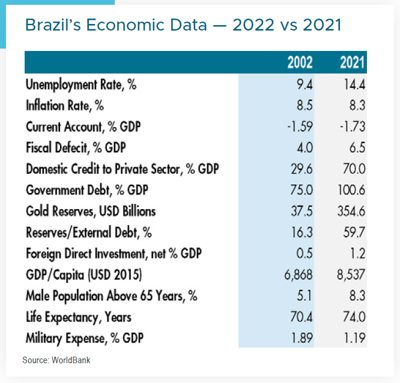

Besides a culturally divided country, Lula starts his third mandate in a country that is burdened with large debt and a population experiencing unprecedented hunger, unemployment, and social inequality. While the independence of the central bank and the level of reserves are bright spots in Brazil, the need for reforms is urgent as China and India continue to build on their track records of reforms and compete aggressively for foreign direct investment and global trade market share.

Important reforms that have been lacking in Brazil include comprehensive labor reforms, social security reforms, and tax reforms, among others. For example, because of the complexities of the Brazilian tax code, a consumer in the city of Sao Paulo who purchases a pair of shoes online might find them being shipped from a Sao Paulo distribution center to a logistics center in a neighboring state, before being shipped back to the consumer’s house in Sao Paulo. This is the kind of inefficiency that arises from decades of not addressing much needed reforms.

Opinions about whether or not Lula is up to the task abound. Some say it will be impossible for him to achieve much with such a fractured Congress, while others point to his previous track record of market-friendly policies as a sign of hope. So far, the returning Brazilian president has given investors more reasons for concern than hope. While he chose moderate Geraldo Alckmin to be his vice president, and has recently bestowed more powers to him, Lula has filled very important cabinet positions, such as the minister of finance, with party loyalists. Investors are left with conflicting messages from Lula’s cabinet daily. While this week we have heard VP Alckmin calling for much-needed tax reform in Brazil, we also are confronted with news of price caps and interest-rate controls in important industries such as oil & gas and the banks.

Meanwhile, India has already reduced its corporate tax rate to below 25%, set in place an industrial policy to address infrastructure issues such as logistics and ports, and is positioning itself to grab a big share of the manufacturing jobs that will be exported from China, as Chinese real wages are expected to continue to grow for the next 10 years.

Can Brazil Shift from Commondity Exporter to Value-Added Exporter?

Brazil, like most Latin American economies, is among the largest commodity exporters globally. They suffered from an overhang in commodity consumption in the past decade after China’s fixed-asset boom drove global commodity prices in the prior decade through 2010. The lack of reforms during the good times has extended Brazil’s dependency on trading commodities and resulted in chronic current-account deficits as exports of value-added goods have lagged. There is a bittersweetness in being called “a nation that feeds the world,” or one of the four top food-producing countries. Relying on commodities gives the country a sense of security that many other emerging economies that lack resources go through periodically. However, that dependence does not generate wealth in the way that gains in manufacturing productivity might.

From 2011 to 2021, China’s GDP per capita more than doubled, and India’s grew by more than 50%, while Brazil’s declined by almost 50%. India and China combined have more than 10 times the population base of Brazil, which makes the divergence even more remarkable.

What Are the Investment Opportunities?

Emerging economies offer natural resources, young populations, cheap labor, and a large consumer market of more than four billion people. However, to translate these into sustainable productivity and real wage growth, governments need to have a long-term relentless commitment towards reforms. Which reforms would help Brazil escape the middle-income trap it’s in now? We believe a combination of tax reforms, industrial policy reforms, social security reforms, and privatizations would help. Unfortunately, we believe the chances are higher that Lula will embrace socialist policies rather than structural reforms, considering the current political environment in Brazil. Thus, we continue to remain skeptical towards Brazil’s ability to join China and India in growing their respective middle classes in a sustainable way.

Our long-term view continues to be shaped by this belief and the growing middle class in Asia. We believe well-run companies with strong brands and sustainable competitive advantages serving emerging market consumers in Asia are likely to continue experiencing solid earnings growth and equity returns.