GW&K Taxable Bond Monthly Commentary - April 2022

GW&K Outlook and Positioning

Volatility should remain elevated in the near term as monetary policy contracts further and geopolitical strains persist. Financial conditions are set to tighten substantially during the remainder of the year, with potentially material consequences for both the consumer and the corporate sectors. Supply chains are also likely to continue to struggle amid geopolitical and COVID uncertainty.

April 2022 Review

The bond market experienced another sharp selloff in April, extending an exceptionally weak start to the year. Increasingly hawkish language from Fed officials heightened already-aggressive expectations for rate hikes and highlighted the FOMC’s commitment to curbing inflation. The war in Ukraine, China’s zero-tolerance COVID policy, and global supply-chain stresses remained overhangs as well, further exacerbating uncertainty.

Fed

Minutes from the March meeting and commentary from officials pointed to an interest in moving “expeditiously” toward a neutral policy rate. The path toward this goal appears likely to include multiple 50 basis point hikes, with a bias toward front loading the policy response. Commentary also suggested that while inflation readings may soon peak, the priority is to act before expectations become entrenched. The futures market reflected estimates of more than 10 additional hikes through year end.

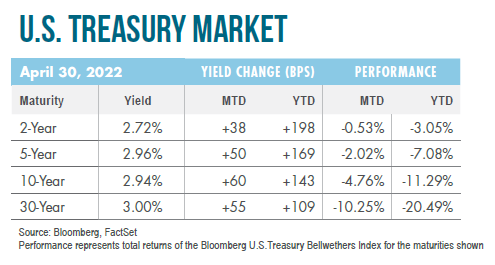

Interest Rates

The yield curve saw a dramatic bear steepening, with most tenors moving decisively to their highest level in more than three years. The front end shifted higher in anticipation of an aggressive course of rate hikes, while intermediate and long rates pushed higher as real rates rose amid tighter financial conditions. Breakevens also drifted higher, reaching record levels as investors continued to grapple with the transitory versus structural question.

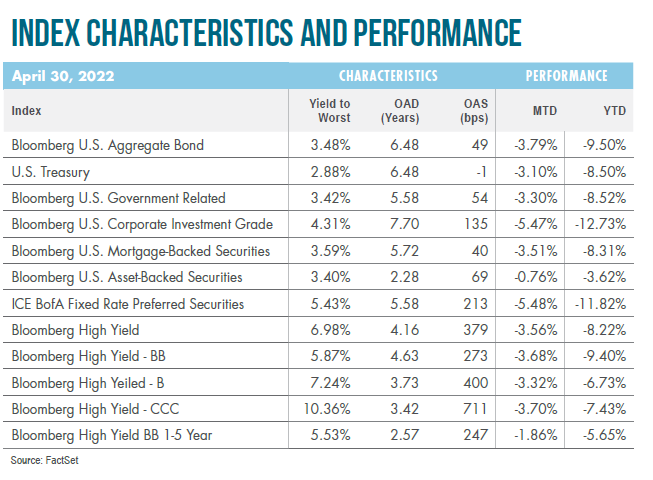

Credit

Corporates were under pressure for most of the month of April, though spreads came up shy of breaking through their March wides. Roughly one-third of companies have reported their first quarter earnings, and for the most part results came in ahead of expectations—particularly in the Energy, Materials, and Consumer Staples sectors. Investment grade issuance remained brisk while the high yield primary market was comparatively subdued. Credit rating agency upgrades outnumbered downgrades as financial profiles broadly continued to improve.

MBS

The mortgage-backed securities market underperformed Treasuries in response to a higher probability of eventual sales from the Fed’s portfolio. Active sales—in contrast to natural roll-off—may be necessary as higher rates have curtailed the speed of prepayments. Lower coupon pools took the brunt of the spread widening due to their high concentration on the Fed’s balance sheet. Quantitative tightening is likely to remain a headwind for the sector until there is more clarity around the pace of balance-sheet reduction.