GW&K Taxable Bond Monthly Commentary — November 2022

GW&K Outlook and Positioning

Fixed income markets rebounded in November on increased confidence that central banks will succeed at taming inflation. Economic data were mixed but fundamentally sound, supporting the prospect of a soft landing.

Fed

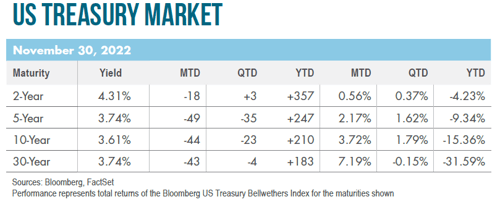

The FOMC raised rates by 75 basis points for the fourth consecutive time while signaling that a slower pace of future hikes would soon be appropriate. The futures market anticipates a terminal rate of nearly 5% in mid-2023, followed by two quarter-point cuts by year end.

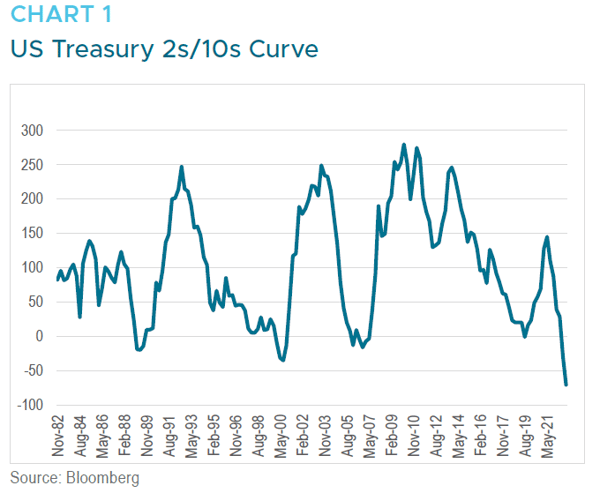

Interest Rates

The yield curve experienced a significant bull flattening, reaching levels of inversion last seen in the early 1980s. The front end rose in response to upwardly-revised terminal rate expectations, while long rates fell on declines in both breakevens and real yields.

Credit

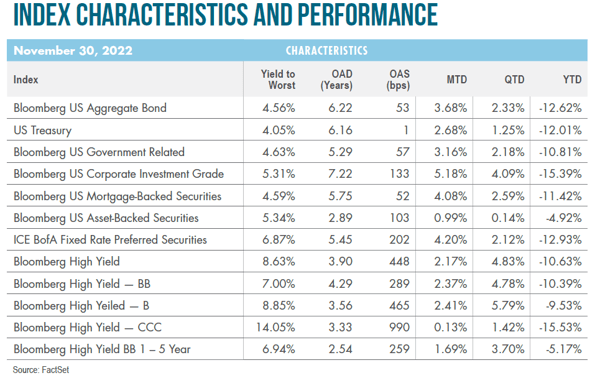

Investment grade spreads saw their sharpest monthly decline in more than two years despite a robust pipeline of new issues. The high yield market posted a second straight month of positive returns, benefiting from an anemic primary calendar and a still-benign default backdrop.

MBS

Mortgage-backed securities outperformed Treasuries, as spreads continued to retreat from post-pandemic wides. Lower-rate volatility, a seasonal decline in originations, and a light maturity calendar from the Fed’s MBS portfolio all contributed to a favorable backdrop.