Municipal Credit Perspectives

Positive Developments for the MTA

The future of public transportation agencies continues to evolve in the aftermath of the pandemic. The sector is facing the dual challenges of tepid ridership recovery against the backdrop of diminishing stimulus funds. However, policy measures impacting the Metropolitan Transportation Authority of New York (MTA) prompted both Moody’s and S&P to issue positive rating actions on the borrower in recent weeks. The strategies employed by MTA may serve as a blueprint for other transit systems seeking to restore fiscal stability.

With New York City as the epicenter of the Covid-19 outbreak, MTA was severely strained by the health crisis. The essential nature of the nation’s largest transit and commuter system is evidenced by the magnitude of federal aid awarded since 2020. Of the $70 billion of pandemic relief provided to the sector, MTA has received $15 billion to date. The emergency funding provided state and local officials a valuable lifeline to keep the system operational, while weighing options to close future budget gaps and fund significant capital needs.

The strategies to restore financial integrity are multi-faceted and include:

- Meaningful increases in state and local tax subsidies

- Resumption of biennial fare increases

- Continued identification of cost efficiencies and savings

- Development of a congestion pricing system to encourage public transit usage and fund capital needs

- Increased reliance on highly-rated debt structures

With federal awards nearly depleted, the State of New York recently increased MTA’s largest single subsidy, the Payroll Mobility Tax (PMT), which is assessed on employers located in the service area’s five boroughs and seven counties. The City of New York also increased its share of operating aid to the agency, while the MTA opted to resume biennial fare increases suspended during the pandemic. The revenue enhancements, coupled with cost savings initiatives, are expected to support balanced operations through 2027, an impressive achievement following consecutive years of dire projections.

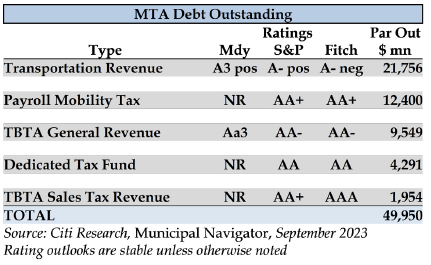

MTA is one of the largest issuers in the municipal market with $50 billion of debt outstanding across multiple indentures, including debt issued by its affiliate system, Triborough Bridge and Tunnel Authority (TBTA). Each debt structure is backed by a distinct security package.

Historically, MTA has funded much of its mass transit and commuter rail capital program through its Transportation Revenue Bonds (TBRs), supported by the gross operating revenues of the network. Beginning in 2020, the agency shifted its offerings to tax-backed debt, including Payroll Mobility Tax and Sales Tax Revenue bonds. The security features of these obligations cause pledged revenues to be first transferred to a trustee for the payment of debt service before remaining taxes are released to subsidize system expenses. The “lockbox” mechanism, which isolates pledged revenues from MTA’s operating receipts, is a structural enhancement that contributes to higher ratings relative to the TBRs. Additionally, MTA has plans to introduce a new type of dedicated revenue structure in 2024, once a congestion pricing toll program is unveiled in Manhattan’s central business district. Budget officials expect the earmarked toll collections will support up to $15 billion of highly rated debt. Given the lower borrowing costs associated with these higher quality credits, MTA officials intend to phase-out TRBs over time, thereby eliminating the impact of operational volatility on bond ratings, while providing significant cost savings.

GW&K owns all five of the MTA’s debt structures listed above and view each as a separate and distinct credit. The collective response of state and local officials to develop a comprehensive balanced operating plan for MTA signals a pivotal turning point for one of the market’s largest issuers. Certainly, we will miss the additional yields offered by the Transportation Revenue bonds but will continue to monitor the authority’s progress in navigating the ongoing challenges in the public transportation sector.

Published October 2023