Municipal Bond Credit Perspectives — 4Q 2022

State of the States: Record Reserves to Cushion Possible Economic Uncertainty

The unique circumstances surrounding the pandemic continue to impact the fiscal condition of the states. Revenue performance over the past two years has been the highest on record, aided in large part by unprecedented levels of federal stimulus. The surprising results have left states flush with cash and well positioned to manage potential economic uncertainty in the coming year.

The primary discretionary operating fund for state issuers is the General Fund. In “normal” years, this account is largely supported by a combination of personal income and sales taxes, although a handful of states do not assess either a personal income tax or a sales tax. In a typical year, the two levies account for about 75% of operating cash.

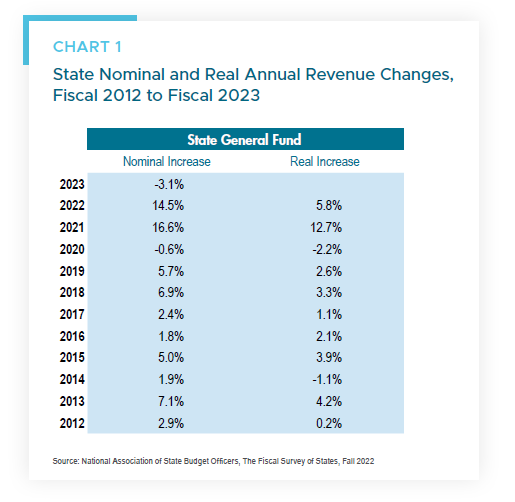

Following historic annual General Fund revenue growth of 16.6% in fiscal 2021, the National Association of State Budget Officers (NASBO) reports in its annual Fiscal Survey of States that operating receipts grew 14.5% in 2022, based on preliminary results. Since its inception in 1979, the Survey has never recorded consecutive years of double-digit percentage gains in sector revenues, with the last period of results above 10% stretching back to 1989. While there is some noise in the recent data due to tax filing delays and the recognition of certain federal aid as operating revenue, the impressive statistics also reflect solid economic and employment growth, a rebound in consumer sentiment, and robust stock market performance in 2020 and 2021. Given the unexpectedly strong performance, it should be no surprise that 49 states reported 2022 collections outpaced budget estimates, with aggregate receipts exceeding original forecasts by 20.5%.

Sizeable windfalls over the past two years prompted 31 states to enact tax cuts in fiscal 2023, while only five adopted net increases. Tax relief efforts ranged from temporary targeted measures to permanent reductions, including some to be phased-in over multiple years. Finance officials are maintaining a conservative tack with forecasts that project sector-wide General Fund revenues will drop 3.1% from 2022 levels. However, recent collections indicate the peer group will experience yet another upside surprise in 2023, as 33 states reveal tax collections outperforming budget estimates.

Given the unusual nature of service demands and associated funding sources during the pandemic, state spending levels exhibited wide swings, with annual operating expense growth of 2.5% in 2021, followed by 18.3% growth in 2022. The unparalleled budget expansion witnessed in 2022 was an anomaly, driven primarily by non-recurring responses to the health crisis, in part subsidized through federal assistance. The $195 billion of funding awarded to the sector via the American Rescue Plan Act is available for use through December 2024 and factors into a somewhat elevated budget growth rate of 6.7% planned for 2023.

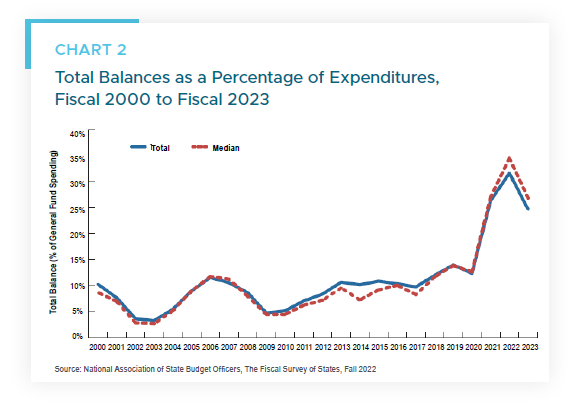

Consecutive years of strong tax performance coupled with significant federal aid have produced extraordinary levels of reserves. Total balances, including “rainy day” reserves doubled in fiscal 2021 and increased again in 2022 to a record $342.9 billion, with the median balance representing nearly 35% of General Fund spending. Remarkably, 46 states exhibit reserves exceeding 10% of expenses. Although budget plans for 2023 indicate many states plan to draw on surplus cash, primarily for one-time investments, the median balance is expected to remain a robust 27% of aggregate spending at year end.

The fiscal health of the peer group is incredibly strong, with all states sharing in the solid performance of recent years. We have been encouraged by the deliberate allocation of generous reserves and expect prudent fiscal practices will continue. As of year-end 2022, we owned 35 different issuers and have added to higher yielding names, including New Jersey and Illinois given measurable credit improvements. Evolving challenges include the expiration of federal stimulus against the backdrop of a slowing national economy, wage pressures, faltering pension plan investment returns and developing constituent needs. We believe the universe is equipped to manage future headwinds and we affirm our stable outlook on the sector.