Insights from our Global Strategist - August 2022

Recession, Contraction, Slowdown? Market Considerations for Investors

The debate about whether the US is in a recession or not continues, with rising inflation and interest rates and high energy costs fueling consumer fears about where the economy is headed, despite near record-low unemployment. We sat down with GW&K's Global Strategist Bill Sterling to ask some recession questions that are top of mind, and to get his take on what investors need to know when making asset allocation decisions in the market environment we're in — whether it will officially be added to the history books as a recession or not.

Are we in a recession?

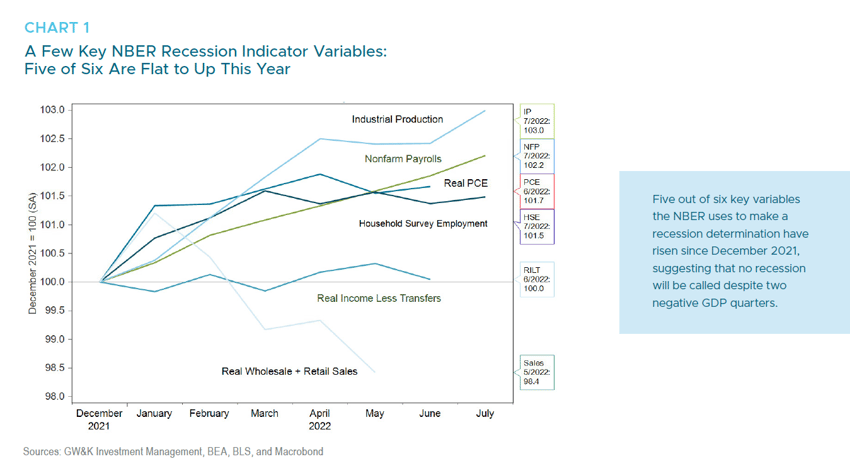

Bill Sterling: Probably not, even though the US real gross domestic product (GDP) declined for two consecutive quarters in the first half, which meets the unofficial definition of a recession. However, an important alternate measure of the size of the economy, real gross domestic income (GDI), expanded at a 1.8% annual pace in the first quarter when real GDP was reported to have contracted at a 1.6% rate. Moreover, five out of six key variables that the National Bureau of Economic Research (NBER) uses to determine recessions either expanded or were flat in the first half of the year (Chart 1). Most notably, nonfarm payroll employment expanded at a very robust average pace of 479,000 per month in the first half, which is hardly what would be expected in a recession.

Against this backdrop, we would not be surprised to see the economic data eventually be revised to erase at least one of the two consecutive quarters of decline in real GDP this year.

What current factors are most likely to keep us out of a recession?

Bill Sterling: There is no doubt that economic momentum has slowed this year, as both consumers and businesses have struggled to cope with high inflation and rising interest rates. That said, corporate and household balance sheets are still strong because of large cushions of excess savings and high cash balances that were built up during the pandemic. Labor income continues to grow at a rapid clip thanks to the tight labor market, which should continue to support both consumer spending and corporate profitability. There are also encouraging signs that inflation is starting to come down as supply chain pressures ease and commodity prices moderate. Particularly helpful to consumers is the drop in gasoline prices of more than $1 a gallon since mid-June. Moreover, despite the rapid pace of Fed rate hikes, interest rates still remain low relative to inflation and cannot yet be considered highly restrictive.

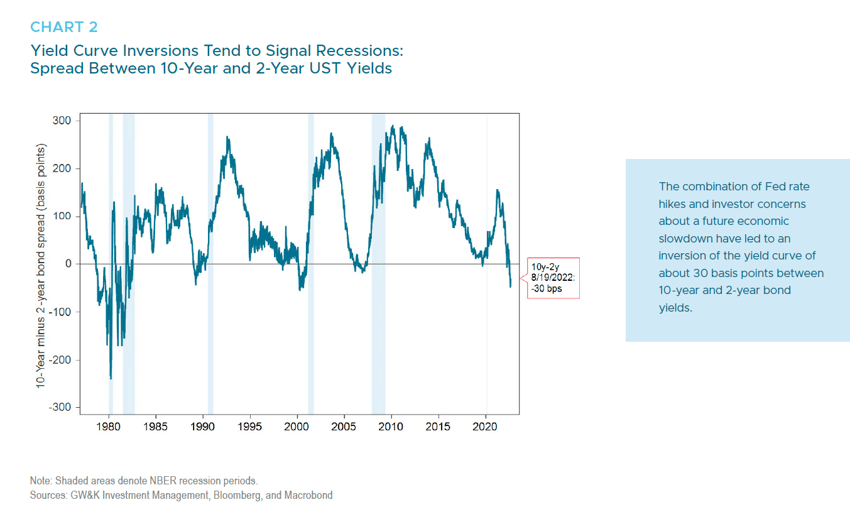

Why does an inverted yield curve signal a recession?

Bill Sterling: Most economic indicators tell us about the recent past, such as growth in GDP, jobs, industrial production, or corporate earnings. But the slope of the yield curve — the difference between long-term and short-term bond yields — provides a window into the future. That’s because it reflects how investors expect developing economic conditions to affect future cash flows from their varying investment options.

For example, suppose investors see the Fed aggressively raise rates and think that will lead to slower growth and lower inflation. The result is likely to be a “flight to quality,” with buying pressure on long-term Treasury bonds driving prices up and yields down. The greater their concerns regarding an economic slowdown, the more likely the yield curve will invert, with long-term rates falling below short-term rates. That is exactly what we have seen recently, with a 3.3% yield on 2-year US Treasury notes compared to a 3.0% yield on 10-year US Treasury bonds.

Are there different types of recessions — such as inflation versus credit? Or are all recessions the same?

Bill Sterling: Most recessions tend to be preceded by Fed tightening associated with its inflation-fighting role. But the key catalysts for recessions have varied considerably, including oil price and other supply shocks in the 1970s, credit restrictions in the early 1980s, the “dot.com” crash in the early 2000s, and the subprime credit crisis in 2007. Most recently, recession came in early 2020 as a “bolt from the blue” due to the pandemic. Even that recession was preceded by a brief inversion of the yield curve in August 2019, although no one would argue that it was caused by prior Fed monetary tightening.

How is inflation related to a recession? What is its impact?

Bill Sterling: Inflation generally reflects excess demand relative to the economy’s productive capacity. Rising inflation is therefore a signal to the Fed to raise interest rates to better calibrate demand with supply. Higher rates tend to throttle back demand in interest-sensitive sectors like housing, autos, and other durable goods. Rate hikes also lead to higher capital costs for businesses, which tend to curb capital spending and hiring plans alike.

Surging inflation raises the risk of recession by increasing pressure on the Fed to hike rates aggressively and to invert the yield curve. Note that not every Fed hiking cycle has led to a recession, but all hiking cycles that inverted the yield curve have led to recessions within one to three years (Chart 2). Not only has the Fed already inverted the yield curve, it has ample incentive to be aggressive since CPI inflation at the start of this cycle — at 7.9% — was the second highest of any postwar hiking cycle. It is against this backdrop that a recent Bloomberg survey of economists indicated that odds are now close to even that the US economy will slip into a recession over the next year.1

What actions does the Fed have to combat inflation?

Bill Sterling: The main tool the Fed has to combat inflation is rate hikes. During the past two cycles it also aggressively used unconventional policy tools such as dovish forward-rate guidance and balance-sheet expansion to support the economy. Therefore, a sharp reversal of those policies has also been part of their tool kit in fighting inflation during the current cycle.

Specifically, the Fed began warning in late 2021 of the potential need to raise rates and reduce its balance sheet. That hawkish forward guidance led to higher market interest rates and tighter financial conditions earlier this year, well in advance of the initial rate hike on March 16. The Fed is also on track to reduce its $8.9 trillion balance sheet at a $1.1 trillion annual rate beginning in September. The intent is to keep upward pressure on bond yields and further tighten financial conditions to help curb inflation.

What does a recession mean for bond investors? Equity investors?

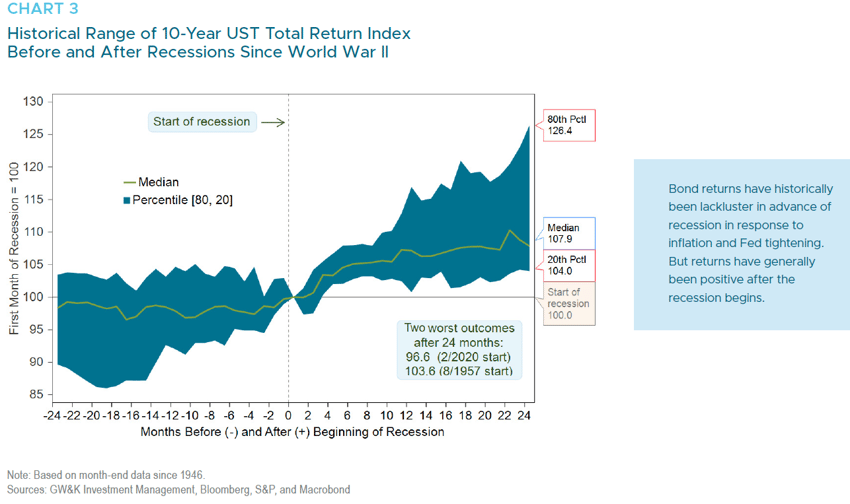

Bill Sterling: Bond investors tend to experience lackluster returns ahead of recessions as the Fed raises interest rates and inverts the yield curve. But in recession periods, the inflation rate typically falls by about one-quarter from its initial level over the next two years. That is usually accompanied by Fed rate cuts, a steeper yield curve, and better performance from bond portfolios (Chart 3).

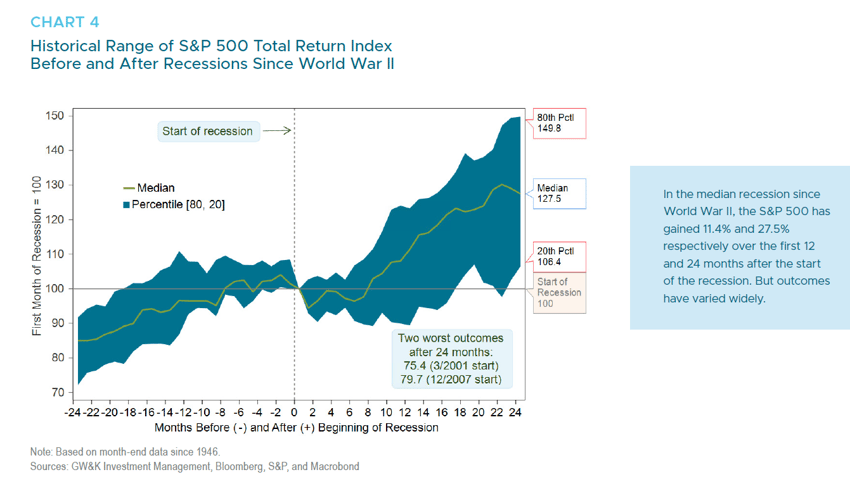

It is harder to generalize about equity markets and recessions, since the range of outcomes has been quite wide. In the typical cycle, equity markets tend to come under pressure in the first six to eight months as corporate earnings decline and economic angst pressures stock valuations. According to Goldman Sachs research, the S&P 500 has contracted by 24% in the median recession since World War II, while S&P 500 earnings have dropped by a median 13%.2

However, those figures tend to overstate the challenges to equity investors during recessions since they focus on maximum drawdowns. In most cases, equity valuations and corporate earnings have responded well to rate cuts in response to recessions. As a result, in the median recession since World War II the S&P 500 posted gains of 11.4% and 27.5% respectively in the following one and two years (Chart 4). Note those market recoveries often occur against the backdrop of terrible economic and corporate news and a torrent of “doom and gloom” stories in the financial media. So investors are often shell-shocked just at the time when excellent investment opportunities open up.

What does this mean for investors' asset allocation?

Bill Sterling: With so much focus in the financial media about recession risks, a key risk for long-term investors is overreacting to the fear factor by trying to aggressively time the market. Markets can behave in very counter-intuitive ways that are impossible to predict. We think most investors are best served by having an “all-weather” asset allocation based on their own circumstances and risk profile.

Unfortunately, recessions are a fact of life, and the economy has been in recession an average of once out of every eight years since World War II. An investor’s asset allocation should recognize that recessions — and market drawdowns — can and do happen. Working with a financial advisor, their portfolio’s risk exposure should be calibrated accordingly. The most important behavioral factor then is to stick to the plan.

1 Vince Golle and Sarina Yoo, “Odds of US Recession Within Next Year Near 50%, Survey Shows,” July 15, 2022.

2 Allison Nathan, “Equity Bear Market: A Paradigm Shift?”, Top of Mind, Issue 109, Goldman Sachs, June 14, 2022.