California's Proposition 2 Provides Guardrails for Future Fiscal Challenges

- After two years of unprecedented revenue growth in the US, many states, including California, are now experiencing tax revenue declines.

- California’s widely publicized budget shortfall has been addressed through a variety of measures — including provisions in Proposition 2, which created new rules for how the state manages its budget, with revisions to how debt, rainy-day fund, and pension plan payments are made.

- We believe California is well positioned to manage future fiscal challenges — despite a potential budgetary shortfall — thanks to Proposition 2 and other recent fiscal policies that have strengthened its balance sheet.

The National Picture

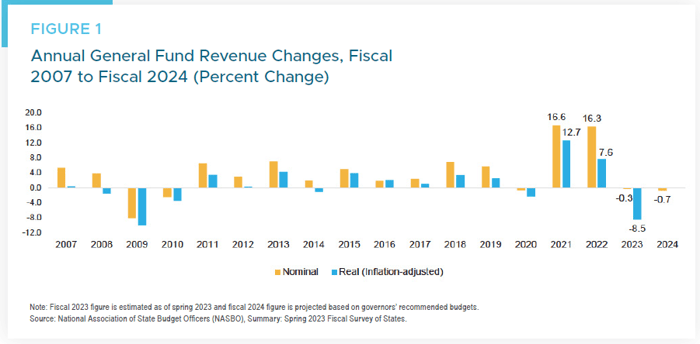

Following consecutive years of unprecedented revenue growth fueled by federal stimulus, states across the US are experiencing tax revenue declines due to volatile market returns, higher interest rates, and a slowing economy.

A recent survey by the National Association of State Budget Officers (NASBO) shows historic revenue performance in state general operating funds for 2021 and 2022, followed by a decline in 2023 and continued weakness expected for 2024 (Figure 1).

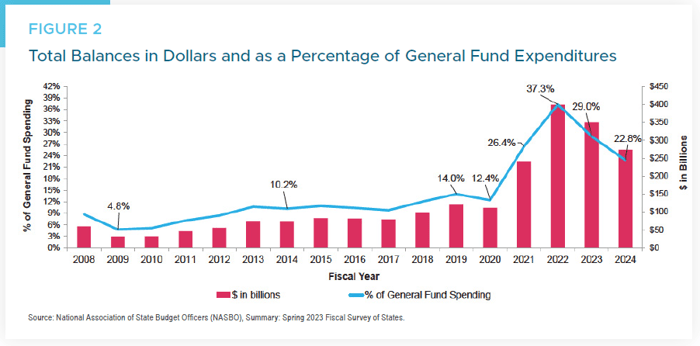

The extraordinary collections over two years were primarily directed to non-recurring pandemic programs, yet revenue performance exceeded expectations and resulted in large surpluses that were tucked away in reserve funds. A recent NASBO survey shows record reserve levels at the end of fiscal 2022. And while state officials plan to draw on these assets, operating reserves at the end of fiscal 2024 are projected to remain quite healthy — well above 2019 levels (Figure 2).

The State of California

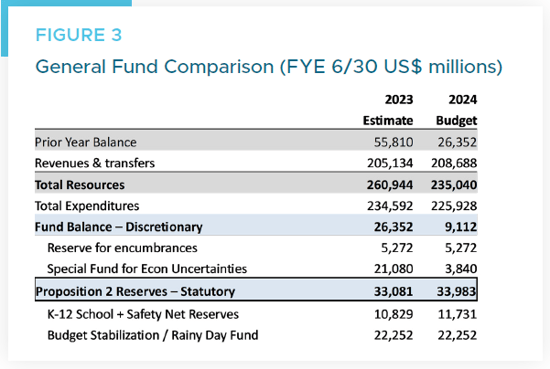

California’s fiscal 2024 budget plan (Figure 3) addressed a significant budget gap that was remedied through a variety of measures. One complication in the 2024 budget process was the tax-filing extension from April 15 (fiscal 2023) to October 15 (fiscal 2024) offered to nearly all counties in the state following disruptions caused by winter storms.

Following two years of exceptional revenue growth, California closed fiscal 2022 with a discretionary General Fund balance of more than $55 billion, or approximately 23% of expenses for the year. Although General Fund revenues (excluding transfers) declined 8% in fiscal 2023 and are expected to remain essentially level in the current year, General Fund revenues remain 40% above 2019 levels of approximately $140 billion.

The final budget plan for fiscal 2024 is a balanced plan based on several solutions, including:

- Spending reductions and delays

- Revenue shifts and internal borrowing from funds outside the General Fund

- Draw down of discretionary reserves

It is important to note that while discretionary balances were tapped to support the 2024 budget, statutory reserves remain untouched and represent a meaningful 14.5% of planned expenses, and the Budget Stabilization Account is currently funded at its constitutional maximum requirement.

What is Proposition 2?

California’s Proposition 2 is a statue passed by voters in 2014 that amended the State’s financial reserve requirements and debt management practices. It addresses California’s progressive tax system and its reliance on volatile capital gains taxes for a portion of its operating revenue.

One of the more important mandates requires a portion of all General Fund receipts and excess capital gains taxes to be placed in a Budget Stabilization Account. Other statutory transfers include reserves for K-12 school programs, traditionally one of the largest budget expenses. Debt management controls include the pay down of liabilities, the prepayment of outstanding debt, and the use of surplus funds to make extra contributions to state pension plans.

In a recent offering statement officials report since fiscal 2018, the State of California has made more than $19 billion of supplemental contributions to its pension plans to improve funding levels and reduce outstanding liabilities.

Key Takeaways

We believe that California is currently well positioned to manage future fiscal challenges. Its broad and diverse economy is the fifth largest in the world, and many lessons learned from the Great Recession have prompted the adoption of fiscal policies that have materially strengthened California’s balance sheet.

Published November 2023