GW&K Emerging Wealth Insights — March 2023

China's New Policies Under Xi's Third Term

China’s National People’s Congress (NPC) will take place from March 5 – 17, and important positions will be filled during this session — such as a new premier and four new vice premiers, the head of the People’s Bank of China, the head of the China Securities Regulatory Commission, and a new head of the China Banking and Insurance Regulatory Commission. Important economic plans will also be announced, including an annual budget for 2023 and an Economic and Social Development Plan. Targets for annual GDP growth, inflation, fiscal positioning, employment, money supply, and total social financing growth will also be set during the NPC.

As crucial as those targets are, equally important are the specific economic and industrial policies that will be announced to support such targets. In recent speeches, President Xi has pointed to the following topics as priorities:

- Upgrading China’s industry — i.e., reducing dependence on the West by narrowing the performance gap in critical areas in technology, manufacturing, industrial automation, artificial intelligence, and green energy.

- Stabilizing the housing market, which is critical to consumer sentiment.

- Narrowing the performance gap and government treatment between state-owned enterprises (SOE) and non-SOEs, which ultimately should mean equal government treatment of SOEs and non-SOEs.

- Supporting consumption — for example, potentially introducing consumer voucher programs and electric vehicle subsidies.

- Restoring market confidence. We expect further reforms from the Chinese government will be required to achieve this.

Will the Chinese Government Put Forward a Broad Consumption Stimulus Package?

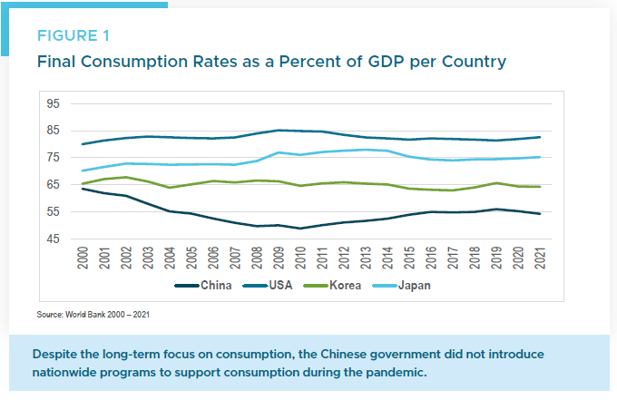

After massively upgrading its fixed-asset infrastructure from 2000 to 2010, the Chinese government set a goal to shift economic growth towards consumption, which lasted until the Covid pandemic started in early 2020. During the pandemic, consumption was negatively impacted by the strict zero-Covid policy that just ended in late 2022. As a result, consumption as a percentage of GDP declined from 56% in 2019 to approximately 53% last year (Figure 1). Even pre-pandemic, these levels are well below 82% in the US, 75% in Japan, and 64% in South Korea.

The build-up of excess savings above trend during the pandemic was also materially lower in China than in the US and Eurozone.1 China is now trying to find the balance between encouraging consumption while at the same time encouraging productivity — which is one reason the government has not provided direct subsidies to consumers on a national scale.

There were a few programs to support consumption during Covid, led by some of China’s wealthier provinces; however, these were very limited in scope and size. At this point there is no consensus as to how broad the consumption stimulus will be and what form it will take in 2023. Despite the inequality of incomes in China, market expectations vary from tax credits for low-income households, educational expense vouchers, general digital yuan (CNY) consumption coupons, elderly care subsidies, EV subsidies. The list of ideas is long. On a longer-term basis, we expect the government to institute policies that provide affordable access to quality health care and retirement benefits, which will reduce the savings rate.

It All Boils Down to Confidence

When focused on the domestic economy, Chinese leaders have the challenging task of balancing the self-inflicted bursting of its real estate bubble with reopening its economy, the need for job creation, further reforms, and the much-needed recovery in both consumer and business confidence.

Recovering consumer confidence levels is tied to both jobs and income growth. As China reopens, there are signs of optimism with respect to jobs. Baidu, a multinational technology company based in China, has recently published datasets which point to a steady return of migrant workers from rural areas to the cities.2 This has traditionally been a leading indicator for future job growth in Chinese cities, and we view it as a green shoot for China’s economic recovery. Additionally, the Chinese government has recently indicated in the local press that as part of its NPC working session it will include a new reform — of itself.

We believe this could support further improvement in both consumer and business confidence. Although no details have been announced, a recent editorial published in Caixin Global3 points to a few main areas of the new government reform:

- Solve the problem of uncoordinated policy initiatives between top and bottom level government entities.

- Address violations of civil rights — this may take the form of having government entities at all level being more responsive to the concerns of citizens.

- Address the role of government: Find the balance between government policy and market economy.

- Reform China’s Social Security system to properly address the country’s ageing population.

- Improve scientific and technological innovation.

The Path to a Consumption-Led Economy Takes Time

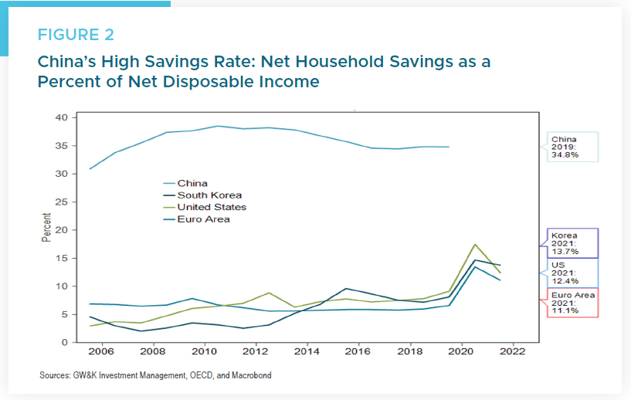

We believe the growth in the Chinese middle class is among the most important investment themes of the next 20 years. However, Chinese households tend to save more than Western households because of the uncertainties resulting from an ageing population, limited investment opportunities, and a market economy with socialist characteristics. It will take time to change these saving habits (Figure 2).

The progress achieved from increasing consumption between 2010-2019 paused during Covid. This progress is now in the process of resuming in 2023. We believe that companies exposed to the rising per capita income and consumption in China will experience strong earnings growth and provide investors with attractive investment returns in the long run.

What Exactly is the Investment Case for China?

China has a large population base of 1.4 billion people. The Chinese people are industrious, motivated, and entrepreneurial, with a very strong work ethic. Like many citizens around the world, the population wants an improvement in lifestyle. This means better living standards for themselves and for their children: higher incomes, better healthcare, financial security, housing, education, and disposable income for goods and services. Over the past 30 years, China has experienced extraordinary growth in terms of per capita income. Hundreds of millions of people have been lifted out of poverty. No matter what specifics come out of the upcoming economic forum, we believe the government of China is committed to improving the living standards of the Chinese people. We also believe that the government is aware that a market-driven economy is the reason for much of China’s economic success over the past 30 years.

The challenge is to find the right balance between a market-driven economy and government controls. If they can achieve this, the economy is likely to grow, lifestyles are likely to improve, and the Communist Party will likely remain in power. As a result, we believe the government is committed to putting policies in place that will help bring GDP growth back to trend. If this happens, China will likely become one of the fastest growing major economies worldwide, with a rising per capita income from the current base of US$12,500.

Domestic consumption is also critical to restoring economic growth, and we believe it will rise to new highs in China over the next 10 years — growing at a pace several percentage points faster than GDP. If this plays out, we believe companies exposed to Chinese consumption will experience faster revenue growth than companies that have no exposure to the Chinese consumer. Since profit margins are well below historic levels, earnings growth will likely be faster than revenue growth. And valuation is currently depressed, with China selling at 11 times 2024 earnings estimates. In our scenario, faster revenue growth for consumer-oriented companies combined with margin expansion and an expansion in their price-to-earnings ratio could result in above-average returns for Chinese equities over the next 5 – 10 years.

Capitalizing on this opportunity will require a long-term view and the ability to withstand volatility. Geopolitical tension, Taiwan, and the Communist Party will be in the news for years to come. But in the end, we believe the government will have to deliver on its promise to improve the lifestyle of the Chinese people. If it fails to do that, it will be game over for the Communist Party. In essence, we believe the headline risk in the short-term will be more than offset by the return potential in the long-term.

1 GW&K Investment Management, Goldman Sachs, and Macrobond

2 Morgan Stanley, China Macro & Consumer Outlook Report, February 12, 2023

3 Caixin Global Editorial: How to Be Problem-Oriented in Institutional Reform. February 27, 2023