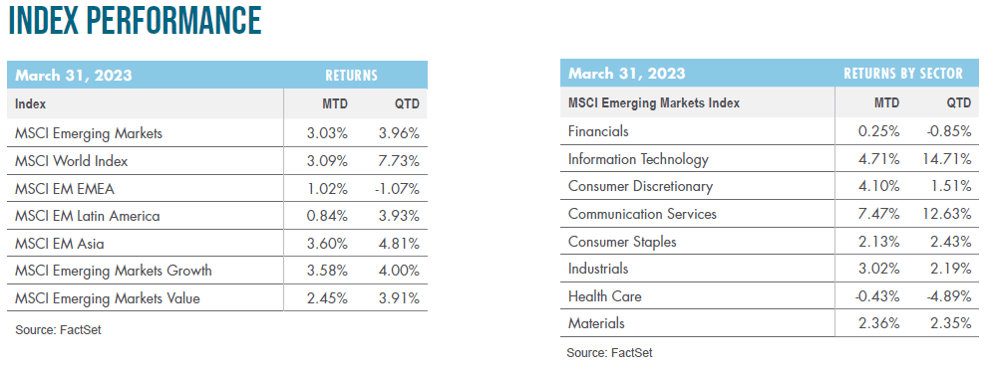

GW&K Emerging Wealth Insights — April 2023

The Case for Global Engagement and Understanding

The United States, China, and India are predicted to be the three largest countries in terms of economic power in the years ahead. According to projections from the International Monetary Fund (IMF), China’s gross domestic product (GDP) is expected to surpass Western Europe’s by 2024, while India and China combined are projected to surpass the US within the next five years (Figure 1). India and China, with their large population bases and rapidly growing economies, are already valuable trading partners and will be increasingly important for countries around the world for imports and exports. Some multinational companies already view them, in terms of GDP and population, as too big to ignore.

.png?width=600&height=371&name=EM%20Figure%201%20-%20GDP%20(USD%20Trillions).png)

While the forms of government are different, the leaders of each country are struggling with many of the same issues. Each country wants an improved standard of living for their population base — including more affordable housing, health care, and education. The cultures are different, but the needs are essentially the same. To remain in power, leadership in each country must deliver economic progress while minimizing corruption and inequality.

Currently it seems that we are living in a world in which all three countries and governments are moving further towards isolation or confrontation, rather than towards global engagement. Choosing engagement could lead to a shared understanding of the needs of each country and how the strengths of each can contribute to the benefit of the others, potentially providing better outcomes for more countries and populations globally.

Energy — China and India's Growing Import Dependency

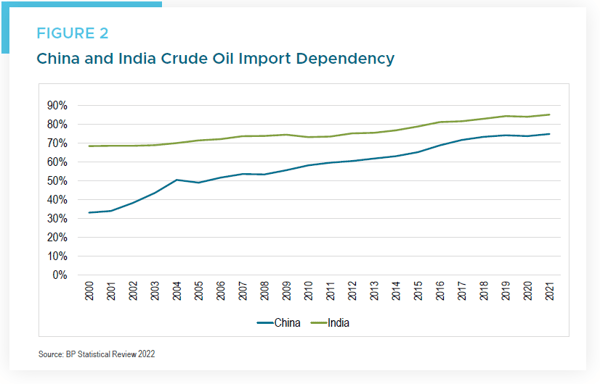

One area that provides a meaningful opportunity for engagement is energy. China and India have long been dependent on imported oil to support their economies. Since 2000, rapid growth and rising per capita income have accelerated these countries’ needs for imported oil.

In 2000, China only imported 30% of the country’s crude oil consumption. While China has made progress on shifting to alternative sources of energy, overall economic growth has outpaced this progress and increased its demand for crude oil. By 2021, China’s imports had increased to over 70% of total crude consumption globally.

India’s reliance on imported oil increased from 70% to more than 80% over the same timeframe (Figure 2). As both countries expect to experience superior economic growth over the next several years, the reliance on imported oil is likely to continue to rise.

China’s energy import cost deficit in 2021 was near the US deficit of $400 billion in 2008, before the US shale oil boom. As the US has reduced its import deficit, China and India’s import deficits have increased materially (Figure 3). India’s goal to be a manufacturing hub will increase its energy needs, and secure sources of crude oil will be critical to both China and India in order to meet their long-term economic objectives.

.png?width=600&height=381&name=EM%20Figure%203%20-%20Energy%20Import%20Cost%20(USD).png)

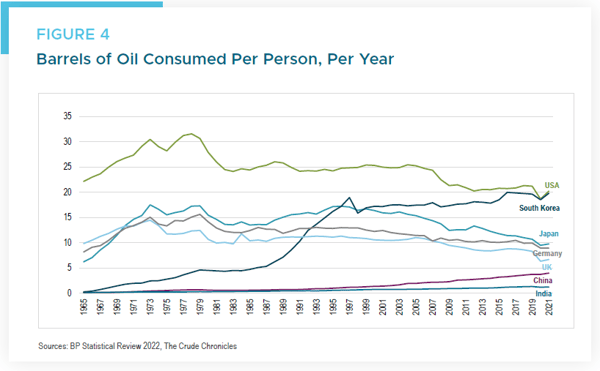

In the US and Europe, energy consumption per capita is declining, but US per capita consumption still remains at four times China’s and nearly 10 times India’s consumption levels (Figure 4). Europe’s consumption is below that of the US but remains well above China’s and India’s. As climate change adaptation grows in importance, energy issues faced by emerging economies, including India and China, will likely increase.

World Order in Transition?

The current world order may be nearing a transition. Geopolitical tensions and supply chain uncertainty have continued to rise over the past few years, and all nations will pay a price if this trend is not reversed. Decoupling and the end of globalization would negatively impact economic growth, productivity, and inflation globally.

India and China represent nearly three billion people. Combined, they are projected to achieve greater economic size than the United States in a few years. Beyond China and India, 87% of the world’s population had no part in making the rules put in place by the G7 nations after World War II, and many of these rules are not necessarily favorable to their sovereign interests. China and India are the two largest nations by population that are emerging rapidly in terms of economic growth. It is likely that a rise in diplomatic, technological, and military power will follow. And, many of the countries outside of the G7 are drawn together by a lack of representation. So, it is possible that we could begin to see a new world order — one that is more inclusive of the most populous nations in the world. Isolation and decoupling would be losing propositions for all countries. We believe engagement, while incorporating an understanding of the history and needs of each country, is the better path forward.

Conclusion

The current investment climate is incredibly challenging. Macro and geopolitical events are already difficult to translate into investment decisions, especially in terms of timing. Even more difficult will be how to determine if the world will evolve towards engagement and understanding or if we continue down the path of isolation.

As always, our plan is to remain focused on our investment discipline. Our portfolio is focused on high-quality companies that benefit from consumption growth in emerging markets in the decades ahead. While geopolitical events will impact volatility in the short term, over the longer term, we believe companies that effectively service consumers in the largest segment of the world economy will produce returns for investors.